Company

Unlock Business Banking

Jamie Verdi

Head of Client Strategy and Partnerships

Every bank and credit union in this country has members who are small business owners. A significant portion of them opened a personal account with you because they trust you — because you are local, because you are theirs. Then they opened a business checking account at the big bank down the street, because that bank had a digital application and you did not.

That is the problem Glide & Q2 are built to solve. And it is more urgent than most institutions realize.

The Business Banking Gap Is a Growth Problem

Banks and credit unions growth has been nearly flat for years. Product penetration — the number of accounts and services a single member holds — is one of the most reliable levers available to reverse that trend. Business accounts punch well above their weight here: they bring in operating deposits, commercial lending relationships, and multi-product engagement that can anchor a member to your institution for decades.

The challenge has always been operational. Business account opening is genuinely more complex than consumer account opening. You have to verify the business entity itself — its legal status, its beneficial owners, its authorized signers. You have to comply with FinCEN's Customer Due Diligence rule. You have to handle sole proprietors differently from LLCs, and LLCs differently from corporations. Most core platforms were not built to do this online. So institutions have been doing it in branch, on paper, and losing members to digital-first competitors in the process.

The window to act is now, and the cost of waiting is not just new accounts lost — it is the deepened relationships that never form.

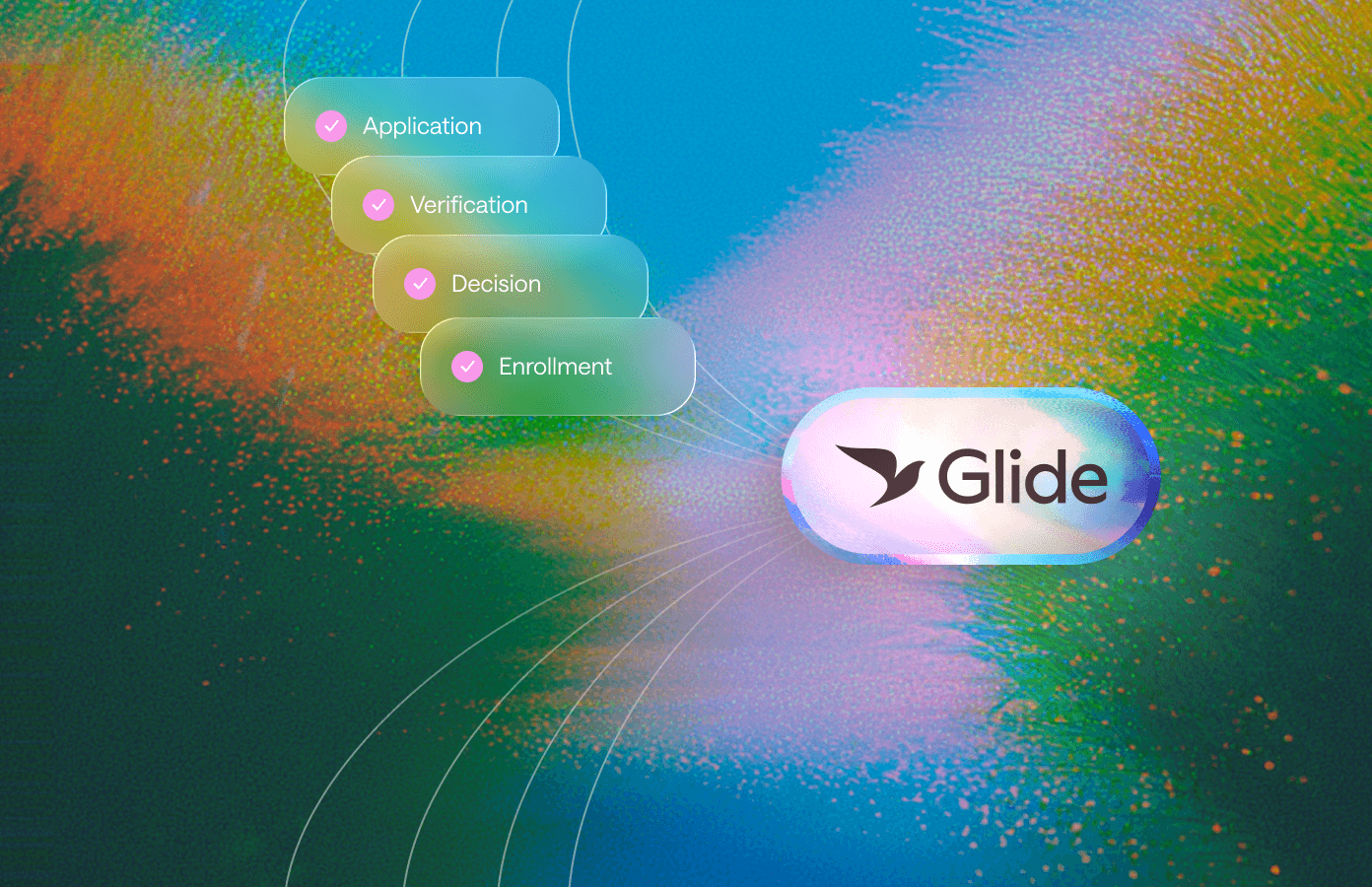

How Glide & Q2 Make Business Account Opening Work

Glide is a digital account opening platform purpose-built for credit unions and community banks. For institutions that run Q2 as their online banking platform, the integration is particularly seamless: when a business member clicks "Open an Account" in Q2, they enter a fully white-labeled Glide flow — no third-party branding, no jarring redirect. It feels like the institution.

The application itself is designed to take under two minutes. Pre-fill pulls in what Glide already knows about existing members, eliminating redundant data entry. The platform supports every major entity type — sole proprietors, LLCs, corporations, partnerships, trusts — and automatically maps the right compliance logic to each one. KYB runs through Middesk, which has direct access to all 50 Secretaries of State + DC, IRS TIN matching, USPS address verification, and OFAC screening. KYC for individual signers and beneficial owners runs through Plaid's IDV and Monitor products. None of this requires a staff member to initiate or manage.

Configurable auto-decisioning means that 70 to 80 percent of applicants get an instant approval. The remaining applications route to a review queue with all the KYB and KYC data already collected, so staff are reviewing — not re-gathering. At the end of the journey, Glide hands the approved account back to Q2 for digital banking enrollment, completing the loop with no manual handoff. Verafin integration flags fraud risk at the point of opening, before accounts are ever funded.

Case Study: What Business Banking at Midwest America FCU Looks Like in Practice

Midwest America Federal Credit Union is one of the most recent institutions to go live with Glide's business account opening product. They run Q2 as their online banking platform and Keystone as their core. The Glide integration sits between both: when a business member initiates an application through Q2, Glide handles the full entity verification flow — all entity types, all signer mapping, Verafin compliance checks — and then passes the completed account back to Q2 for enrollment.

Business members who start the application finish it in an average of two minutes. Accounts are funded and enrolled in digital banking on day one in over 95% of cases.

Results Worth Talking About

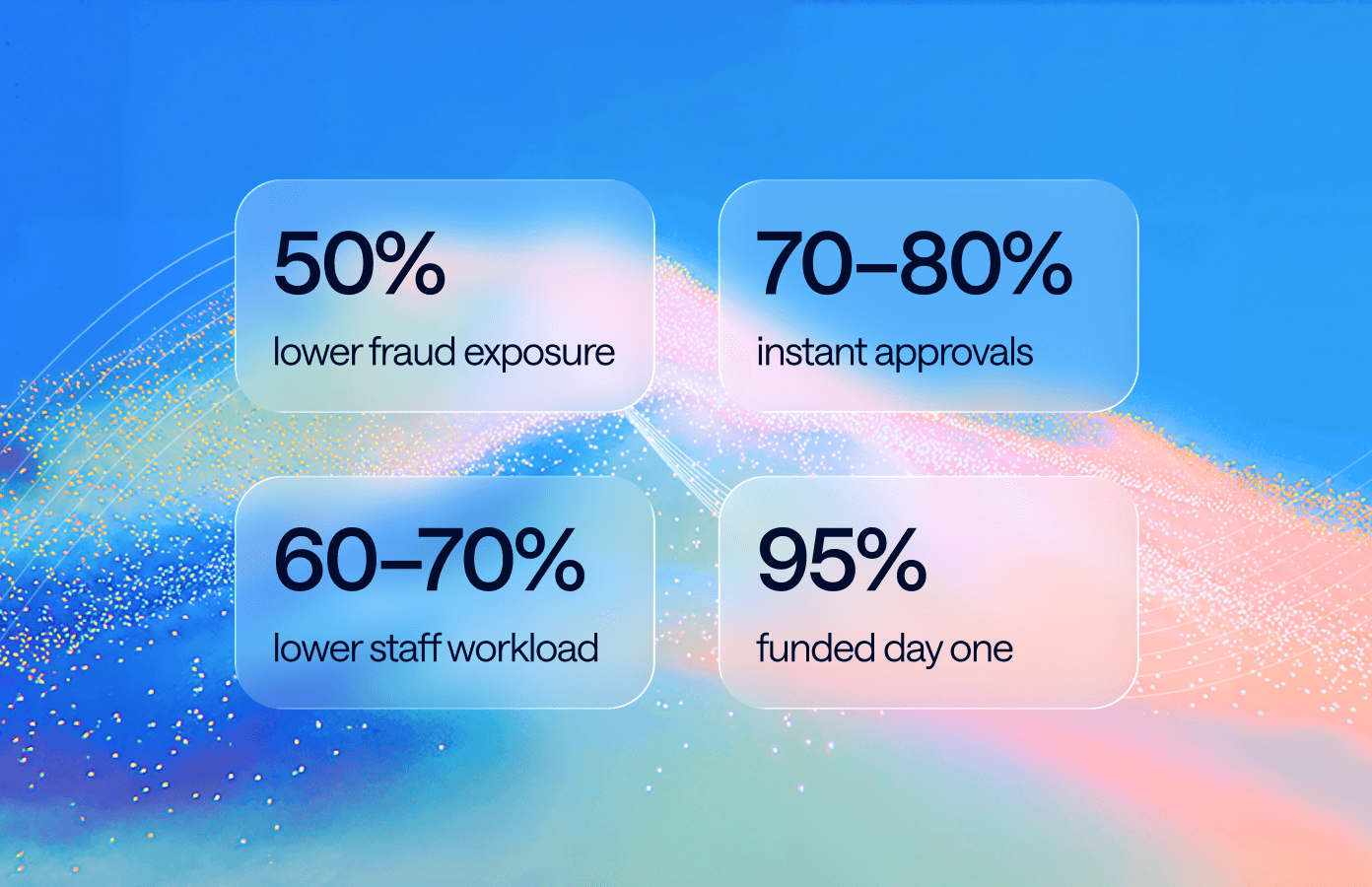

Across Glide's client base, the outcomes have been consistent enough to speak to confidently. Fraud exposure drops by roughly 50 percent when Plaid-powered identity verification is layered in at the point of application — synthetic identities and shell businesses are caught before any account is opened. Staff workload drops by 60 to 70 percent compared to manual paper-based processes. And because auto-decisioning handles the majority of applications instantly, the member experience improves at the same time internal costs go down.

The broader business case is a product penetration argument: institutions that open business accounts grow net new relationships with members who were already trusting them personally. Business checking anchors a deposit relationship. That relationship creates the natural next conversation about commercial lending, merchant services, and treasury management. None of that happens if the business account opening experience is slow, paper-heavy, or simply unavailable online.

Taking Action with Q2 and Glide

If your institution runs Q2, the path to business account opening is shorter than you probably think. The Q2 SSO configuration, the enrollment handoff, and the online banking integration are all well-documented snd ready to go!

The conversation worth having is not "should we offer business account opening online" — the answer to that is clearly yes. The conversation worth having is about configuration: which entity types to support at launch, what your auto-decisioning thresholds look like, how you want to handle the review queue, and what your go-live timeline needs to be.

If you'd like to see how it works in practice, reach out to your Glide account executive or visit Glide to book a demo. The program can be live inside six to eight weeks.

What This Adds Up To

Your members already have small businesses. Some are freelancers, some run LLCs, some have incorporated. They are not asking you to solve a problem they do not have — they are asking you to meet them where they already are. The banks and credit unions doing this well are not the ones with the biggest balance sheets or the most marketing spend. They are the ones that made it easy to say yes to a business account at 10pm on a Tuesday, from a phone, in two minutes. That is the standard Glide is built to help you meet.